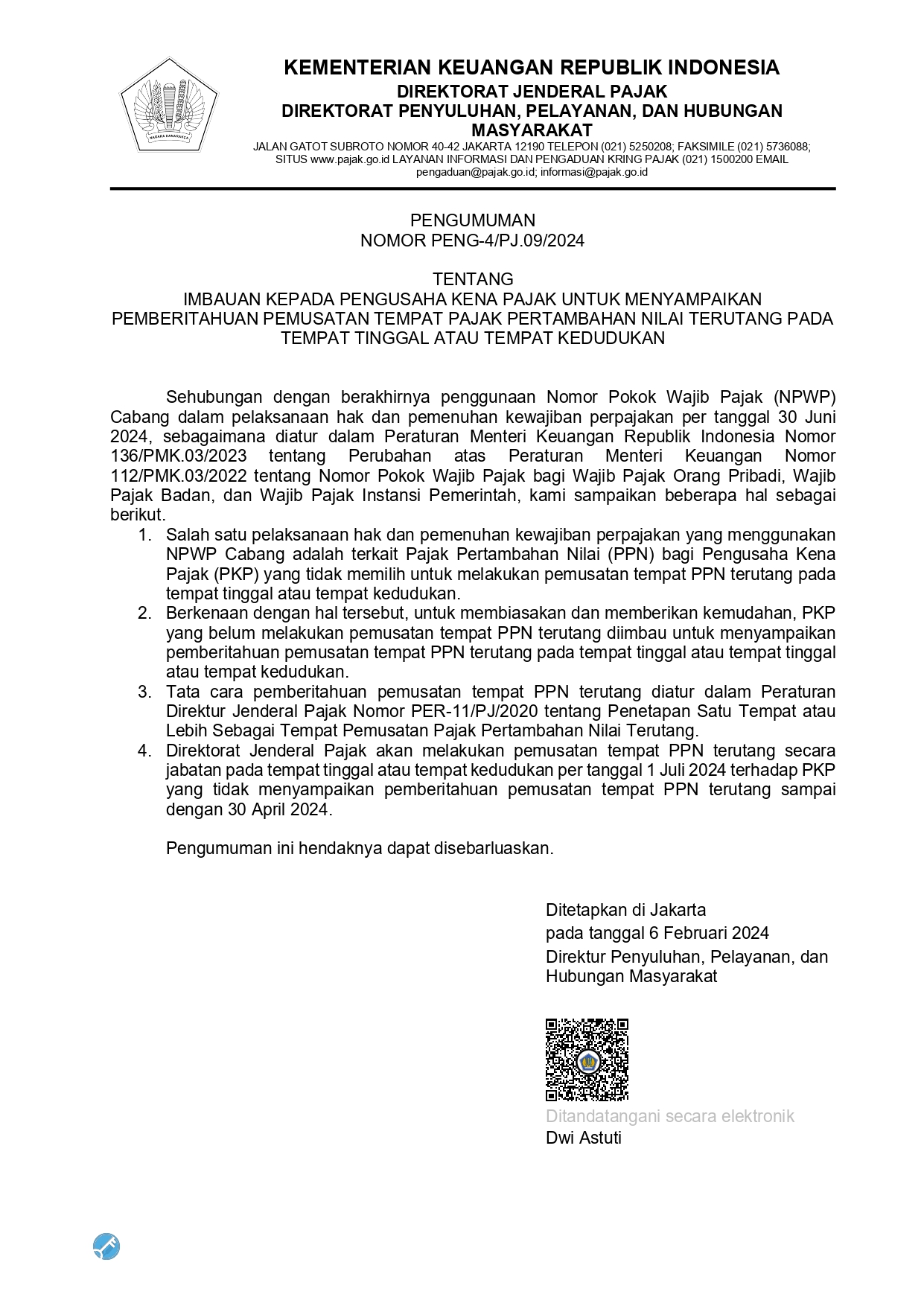

Hello, is there anything we can help?

Tax flash: PMK 47 of 2024 on the Third Amendment to Minister of Finance Regulation Number 70/PMK.03/2017 on Technical Guidelines on Access to Financial Information for Tax Purposes

In mid-August 2024, the government stipulated Minister of Finance Regulation No. 47 of 2024 on the Third Amendment to Minister of Finance Regulation No. 70/PMK.03/2017 on Technical Guidelines on Access to Financial Information for Tax Purposes. Although it was stipulated in mid-August 2024, this provision will only be effective on August 6, 2024.

In the consideration, it is stated that one of the objectives of the enactment of this Minister of Finance Regulation is to provide legal certainty for Financial Services Institutions (FSIs), Other Financial Services Institutions (FSIs), and/or other entities in submitting reports containing financial information for tax purposes.

In addition, another purpose of enacting this provision is to regulate anti-avoidance measures in accordance with the Common Reporting Standard, which requires adjustments to the provisions regarding technical guidelines for accessing financial information for tax purposes.

Several provisions have been amended in this provision. One of them is the addition of Article 10A between Article 10 and Article 11, which, among others, regulates that the reporting financial institution is not allowed to serve the opening of New Financial Accounts for individuals and/or entities that refuse the Financial Account Identification Procedure. In addition, the reporting financial institution is also prohibited from providing new transaction services related to the Financial Account for the owner of the Old Financial Account for individuals and/or entities that reject the Financial Account Identification Procedure.

Transactions as referred to in Article 10A, among others, also include the following four transactions:

- deposit, withdrawal, transfer, account opening, or contract creation for banking customers;

- account opening, purchase or transfer transactions for capital market customers;

- closing of a new policy; and

- other transaction activities for existing financial account holders at reporting financial institutions are those of other financial institutions and/or entities.

Based on the above provisions, it can be interpreted that the reporting financial institution is prohibited from providing its services to customers who refuse to permit financial service institutions and other financial service institutions to report their data to the Directorate General of Taxes.

However, the provision also regulates transactions that are allowed to be carried out even though the account holder refuses the identification procedure, including the following transactions:

- fulfillment of obligations that have been previously agreed between the Old Financial Account owner and the reporting financial institution;

- account closure; or

- fulfillment of obligations based on the provisions of laws and regulations.

In addition to adding to the previous provisions, PMK 47 of 2024 also deletes several articles previously regulated in PMK 70 of 2017. Some of the deleted articles are Article 7, Article 13, Article 14, and Article 24A. However, between Article 30 and Article 31, Article 31A related to anti-avoidance is inserted.

Based on the article, among others, stipulates that every person including Financial Services Institution (FSI), Other FSI, Other Entity, head and/or employee of FSI, head and/or employee of Other FSI, head and/or employee of Other Entity, Individual Financial Account Holder, Entity Financial Account Holder, service provider, intermediary and/or other party is prohibited from agreeing and/or practice with the intention and purpose to avoid the obligations as stipulated in the laws and regulations governing access to financial information for tax purposes.

In addition, the provision also stipulates that in the event of an agreement and/or practice with the intention and purpose of avoiding the obligations as stipulated in the laws and regulations governing access to financial information for tax purposes, the following provisions shall apply: such agreement and/or practice shall be deemed not to apply and/or not to have occurred; and the obligations as stipulated in this Ministerial Regulation shall still be fulfilled by every person, including the Financial Services Institution, Other Financial Services Institution, Other Entity, head and/or employee of the Financial Services Institution, head and/or employee of Other Financial Services Institution, head and/or employee of Other Entity, Individual Financial Account Holder, Entity Financial Account Holder, service provider, intermediary, and/or such other party.

Related Provisions:

- Minister of Finance Regulation Number 70/PMK.03/2017 on Technical Guidelines regarding Access to Financial Information for Tax Purposes.

- Regulation of the Minister of Finance Number 19/PMK.03/2018 on the Second Amendment to Regulation of the Minister of Finance Number 70/PMK.03/2017 on Technical Guidance on Access to Financial Information for Tax Purposes has not yet regulated anti-avoidance provisions by the common reporting standard, so it is necessary to make amendments