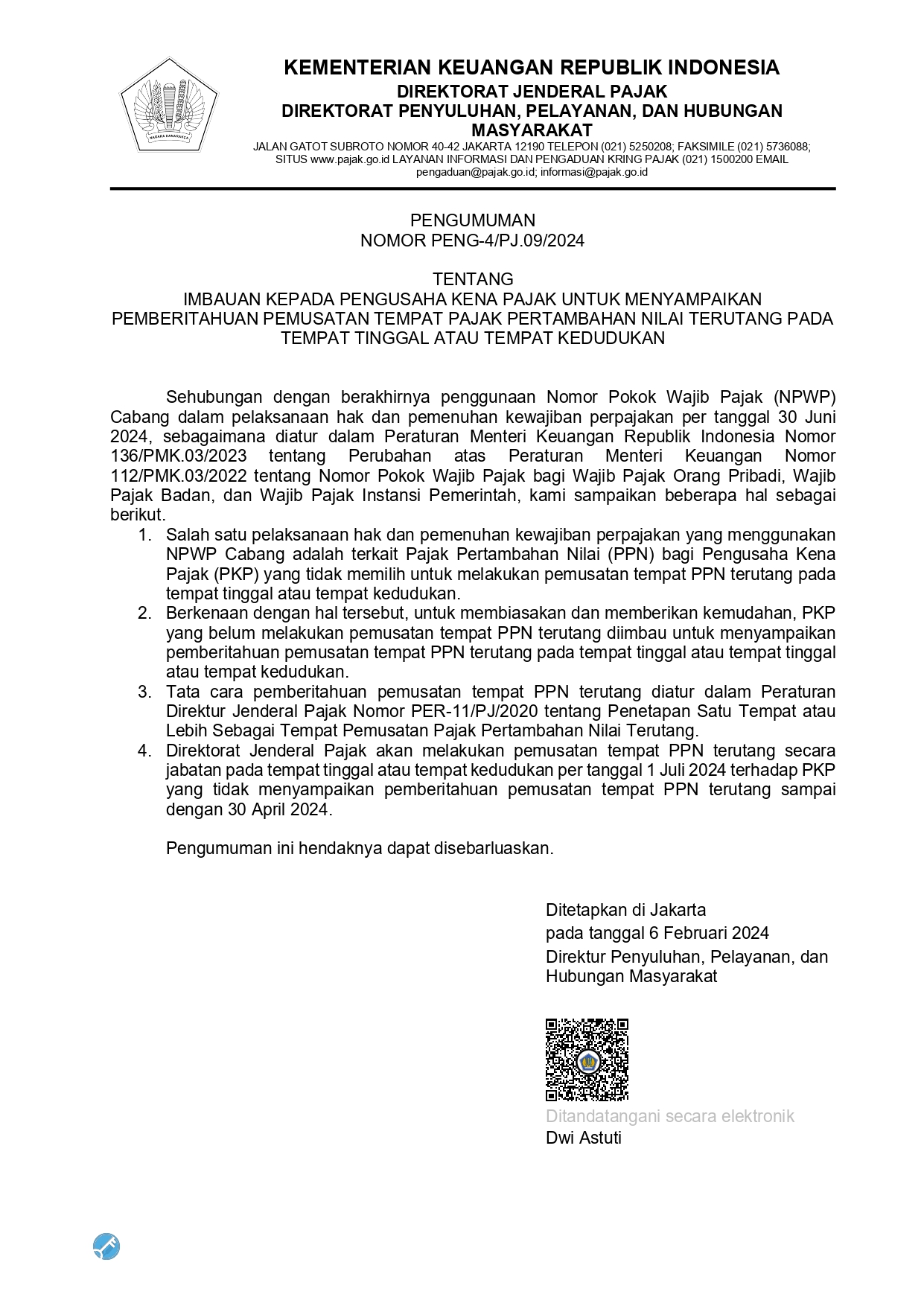

Hello, is there anything we can help?

Minister of Finance Regulation Number 72 Year 2023 concerning Depreciation of Tangible Assets and/or Amortization of Intangible Assets

On July 13, 2023, the Government issued Minister of Finance Regulation Number 72 Year 2023 concerning Depreciation of Tangible Assets and/or Amortization of Intangible Assets.

This regulation is a derivative rule of Law Number 7 of 2021 concerning Harmonization of Tax Regulations and Government Regulation Number 55 of 2022 concerning Adjustment of Regulations in the Income Tax Sector.

This regulation also renews three previous Minister of Finance regulations:

-

Minister of Finance Regulation Number 248/PMK.03/2008 concerning Amortization of Expenditures to Acquire Intangible Assets and Other Expenditures for Certain Lines of Business.

-

Minister of Finance Regulation Number 249/PMK.03/2008 concerning Depreciation on Expenditures to Acquire Intangible Assets Owned and Used in Certain Lines of Business as amended by Minister of Finance Regulation Number 126/PMK.011/2012 concerning Amendment to Minister of Finance Regulation Number 249/PMK.03/2008 concerning Depreciation on Expenditures to Acquire Intangible Assets Owned and Used in Certain Lines of Business.

-

Minister of Finance Regulation Number 96/PMK.03/2009 concerning Types of Assets Included in the Group of Non-Building Tangible Assets for Depreciation Purposes.

This regulation consists of 34 Articles divided into 8 Chapters. The first chapter contains General Provisions. The second chapter contains the Depreciation of Tangible Assets. The Third Chapter discusses the Amortization of Intangible Assets. Chapter Four discusses the Depreciation of Tangible Assets and/or Amortization of Intangible Assets Owned and Used in Certain Business Fields. Chapter Five reviews the Procedures for Application for Approval and/or Notification to the Director General of Taxes. Meanwhile, transitional regulations and closing regulations are discussed in the sixth and seventh chapters.

In general, this provision regulates that there are two methods of depreciation that can be recognized fiscally: the straight line and the declining balance method.

The straight-line method is performed by dividing expenditures for the purchase, establishment, addition, repair, or alteration of tangible assets, except land with the status of ownership rights, building use rights, business use rights, and use rights, which are owned and used to obtain, collect, and maintain income that has a useful life of more than 1 (one) year with a predetermined useful life.

On the other hand, the declining balance method is calculated by applying depreciation rates on the residual book value in each year and at the end of the useful life the residual book value is depreciated at once. Both methods mentioned above can be used as long as they are applied with the principle of principle. The depreciation rates for the straight-line and declining balance methods are as follows:

Unlike the previous provision, PMK 72 of 2023 regulates that if a permanent building has a useful life exceeding 20 (twenty) years, then there are two options for taxpayers in calculating depreciation: using a useful life of twenty years as in the previous regulation or using a useful life in accordance with the actual useful life, provided that they comply with the principle and submit a notification to the DGT.

Notification to the DGT as mentioned above, must be submitted before April 30, 2024. For taxpayers who have submitted the notification, the calculation of depreciation expense for Fiscal Year 2022 is carried out in equal parts over the remaining actual useful life based on the taxpayer's bookkeeping.

In the event that the taxpayer makes improvements to tangible assets and the improvements increase the useful life of the tangible assets, then the useful life is recalculated by adding up the remaining fiscal useful life with the additional useful life due to the improvements. However, it should be noted that the total useful life may not exceed the useful life of the tangible asset group, except for permanent buildings.

This provision also regulates that in the event of a transfer or withdrawal of assets that receive insurance reimbursement, the amount of the remaining fiscal book value of the transferred or withdrawn assets shall be charged as a loss and the amount of selling price and/or insurance reimbursement received or obtained shall be recorded or recognized as income in the year of the withdrawal.

Similar to depreciation, this provision also regulates that there are two methods of amortizing intangible assets: the straight-line method and the declining balance method. The straight-line method is calculated by dividing the acquisition value of intangible assets by the useful life in equal parts. While the declining balance method is calculated by multiplying the acquisition price or book value by the amortization rate and at the end of the useful life amortization is carried out in a lump sum. The amortization rates are as follows:

In the event that intangible assets have a period of benefit exceeding twenty years, the taxpayer may choose to use the useful life according to group four or use the useful life in accordance with the actual useful life provided that it is done in a manner of compliance and submit a notification to the DGT.

There are three specific business fields that can conduct depreciation not at the time the asset is acquired, but during the month of commercial production of the asset. The three business sectors include:

-

Forestry business sector, namely the business sector of forests, forest areas, and forest products whose plants can produce multiple times and only produce after being planted for more than 1 (one) year;

-

Hard plantation business sector, namely plantation business sector in which plants can produce multiple times and only produce after being planted for more than 1 (one) year;

-

Livestock business sector, namely the livestock business sector which includes: livestock business sector in which livestock can produce multiple times and only produces after being raised for more than 1 (one) year; or livestock business sector in which livestock can produce multiple times and already produces after being raised for less than or up to 1 (one) year.

Minister of Finance Regulation No. 72 of 2023 is effective upon promulgation. For non-building tangible assets that have been depreciated in accordance with the useful life of Groups 1, 2, 3 and 4 based on PMK 96/PMK.03/2009, the depreciation period remains valid until the end of its useful life. Except, for the type of non-building tangible assets acquired before the effective Fiscal Year of PMK 72 year 2023 and not listed in the Appendix of PMK Number 96/PMK.03/2009.